The Capital Stack

Our Underwriting Process

Welcome to many new subscribers! For those who’ve been reading consistently, you may ask, “Tory, why am I getting your newsletter at ~8:00pm EST on a Friday night? I’m used to getting it on Thursdays.” Well we’ve been buried with our closing for Suburban 36 which closes on Monday. The seller just got back this week from 3 weeks in India so communication was slow and a lot had to get done in this past week.

In response to a readers request, this week’s newsletter will highlight some of our underwriting process. Our underwriting process remains consistent and has changed very little since our first acquisition. We have used and will continue using the model created by Real Estate Lab and David Toupin. We will review the model and provide a walk through youtube video as part of next week’s newsletter. For now, Let’s look at our buying metrics and what returns we expect on renovations for “Value Add” properties.

Location

We like to buy B Class properties in A/B Class locations. Generally, we can achieve this by purchasing in areas where the median home value exceeds $250,000 and the median household income exceeds $60,000 a year.

When purchasing in a new market we also need to make sure there is a reputable management company in the area that is willing to take on the new property. By focusing on purchasing properties in the same general location (Southeast Michigan), we can achieve economy of scale and eliminate the hassle of working with multiple property management companies.

Lastly, we ask ourselves “would we enjoy living here?” we find it hard to get excited about purchasing a property that we would not live in ourselves.

Current Rent Vs Market Rent

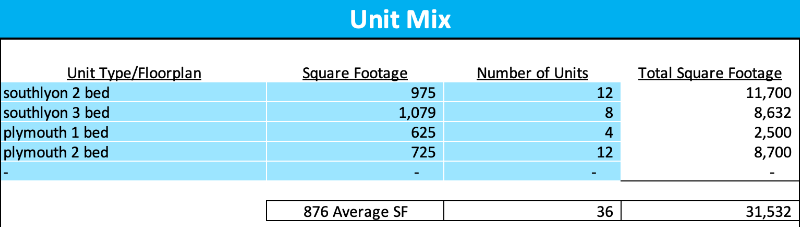

When analyzing the current rent and projecting the market rent brokers will often compare units by the number of bedrooms. We feel this leaves a large margin for error and we choose to determine the price per SF of each unit type. A 1200sf 2-bedroom unit is drastically different and commands a premium over an 800sf 2-bedroom unit. We want to be sure we differentiate between the two.

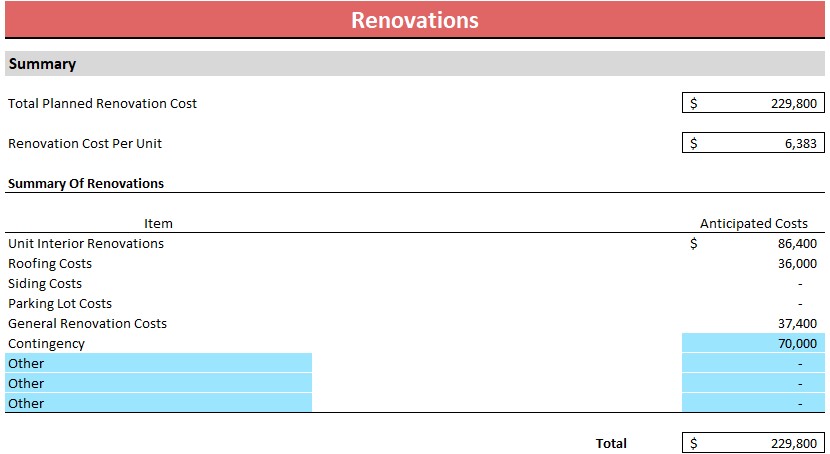

Renovation cost/deferred maintenance

We will typically target a 30%+ return on our renovation costs. The model we use allows us to key in our renovation budget and provides us with a renovation ROI.

- All in reno in an A area ~$20k – target premium $500/month

- All in reno in a B area ~$15k – target premium $375/month

- Reno w/o appliances ~$10k – target premium $250/month

- Reno w/o cabinets/counters ~$6k – target premium $150/month

We also include a deferred maintenance budget. When applicable this budget includes repair or replacement of roofs, parking lots, sidewalks, landscaping, gutters, HVAC, etc. We will typically plan for ~$2000 per unit in contingency cost for uncertain items that pop up. When we get a unit that needs more work than planned, we want to be prepared and not strapped for cash.

Returns

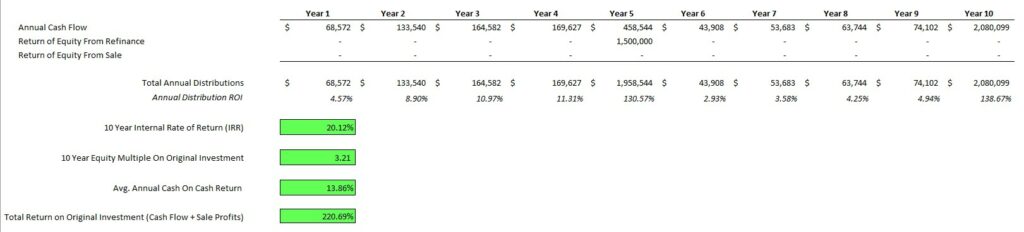

Returns are the most important part for us and our investors. We will not purchase a property if the returns do not meet our standards. We want to hit 15%+ IRR over 10 years. We typically buy with a goal to refinance and return 50%+ of our investor’s original investment in 2-5 years. We purchase properties with the intent to hold them for a long time. This provides a continuous tax benefit for our investors and uses inflation to our benefit. After the value-add program is completed we can be relatively hands off while continued inflation does the bulk of the work to reap benefits for our investors. Inflation from 1960 to 2021 averaged 3.8% and rent has increased 8.86% on average since 1980.

_____________________________________________________________

Hypothetical inflation/rent growth calculation over 10 years:

*This is unrealistic to project as it’s not this simple, but using averages mentioned above for calculations

Purchase property for $5,000,000.

Gross Income $600,000

Expenses $300,000

Net Income $300,000

After 10 years of rent growth & inflation

Gross income $1,369,145

Expenses $435,606

Net Income $933,539

New property value: $15,558,983

Obviously this is wildly favorable and semi unrealistic to project, but crazier price jumps have happened over the last ~10 years and even more dramatic in markets like Phoenix and Texas.

Point is, keeping up with historical average rent growth and inflationary costs over a long term period, rent growth will exceed cost growth resulting in higher values. We target 3-5% rent growth and everything over is a bonus. Several properties we own have had 20% YOY rent growth in the last 2 years which is wildly unrealistic to project but great bonus for our investors.

Major Market News

| Millennials and Renting In a rental market dominated by millennials and being a millennial myself I have a good understanding for what the rental market desires. According to an article by Cort “The rental economy is on the rise. Fueled in large part by millennials”. The article references a recent study and says “Research suggests that more than 50 percent of all buyers would rent instead of own if the items are on-trend. Among millennials, that number goes up to 70 percent.” Check out the article for more information on millennials and the rental market https://www.cort.com/ideas-and-inspiration/lifestyles/generation-rent. |

| Tips and Tricks |

| Check out These Terms: Underwriting Process- Our underwriting process starts by gathering all of the information we can on a property. Our primary focus is: Exact location Year built Number of units Unit mix (studio, 1, 2, 3 bed) Unit square footage Current rent Market rent Once we have all of this information we are able to calculate what the current value is and what the future value is. Keep in mind this relies on many assumptions regarding cap rates but we typically buy with the “refinance when favorable and hold” model so fluctuating property values in short term have very little effect on us. We are more focused on rent growth and expenses. Renovation ROI- Renovation ROI (Return on Investment) on projects we have done has ranged from 20% to over 200%. as mentioned earlier, we target 30% and anything greater just means we’re getting a phenomenal return on the renovation expenses. |